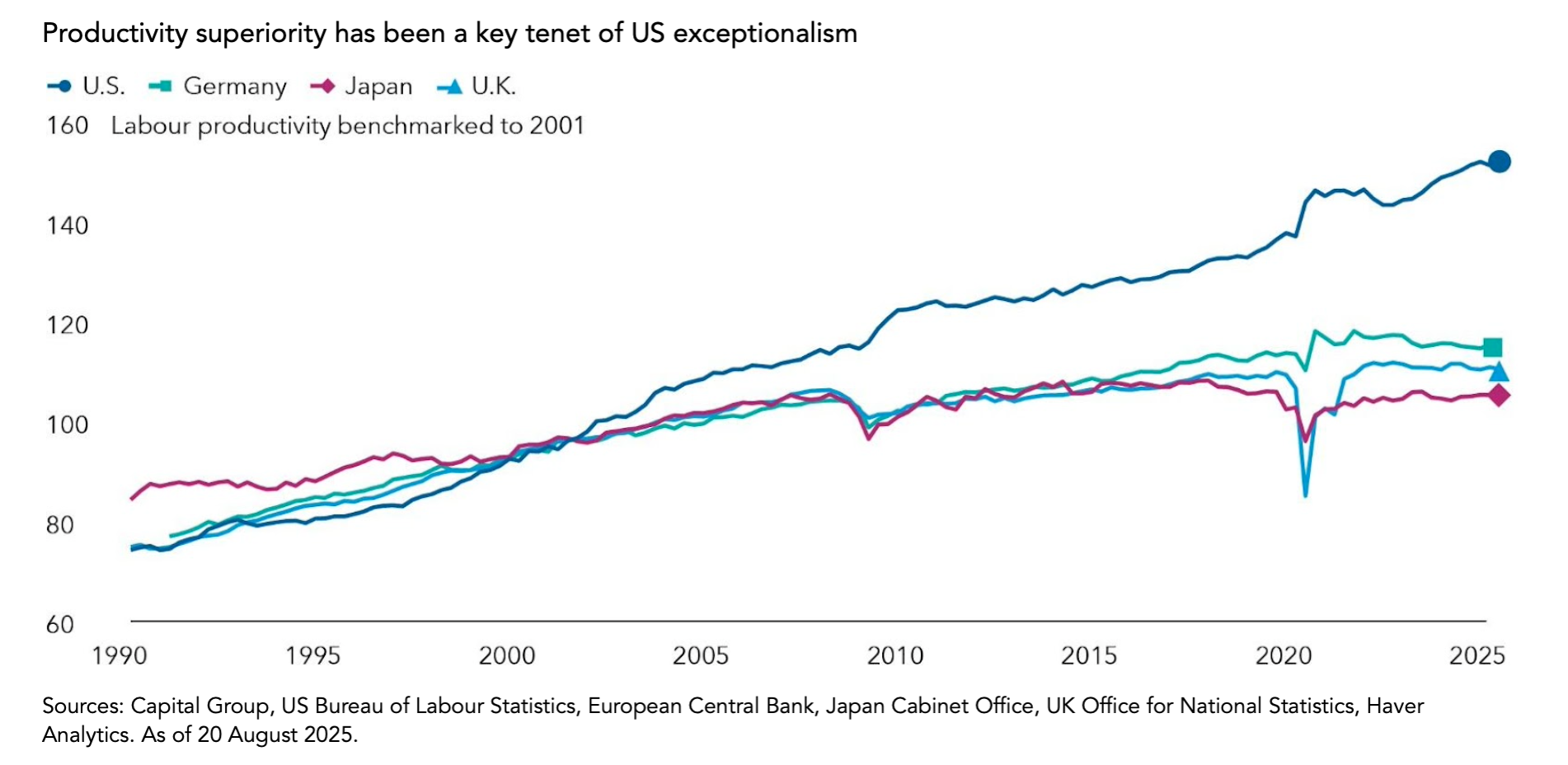

It goes without saying that the US has been a dominant force in the global economy. The structural foundations of its long-term economic growth included a winning combination of superior productivity, a culture of innovation and risk-taking, and a stable, predictable regulatory framework.

Innovation, rapid tech adoption, and flexible reallocation of labour and capital have underpinned the US’s impressive productivity growth since the late 20th century. This compares favourably to Europe which has faced declining productivity, particularly since the Global Financial Crisis, due to lower investment in technology and structural rigidities. Japan has also struggled since the 1970s with a need to invest in digitisation to boost productivity. And while China achieved significant productivity gains as it transitioned from an agrarian to a manufacturing economy, maintaining such strong growth will depend on innovation and efficiency improvements.

As we look ahead, Artificial Intelligence (AI) is emerging as a transformative force.

Historically, several technological breakthroughs have revolutionised industries and significantly boosted productivity. The steam engine, electricity, the internal combustion engine, semiconductors, and the internet are prime examples of General Purpose Technologies (GPTs) that have reshaped economies. AI is anticipated to join this illustrious list.

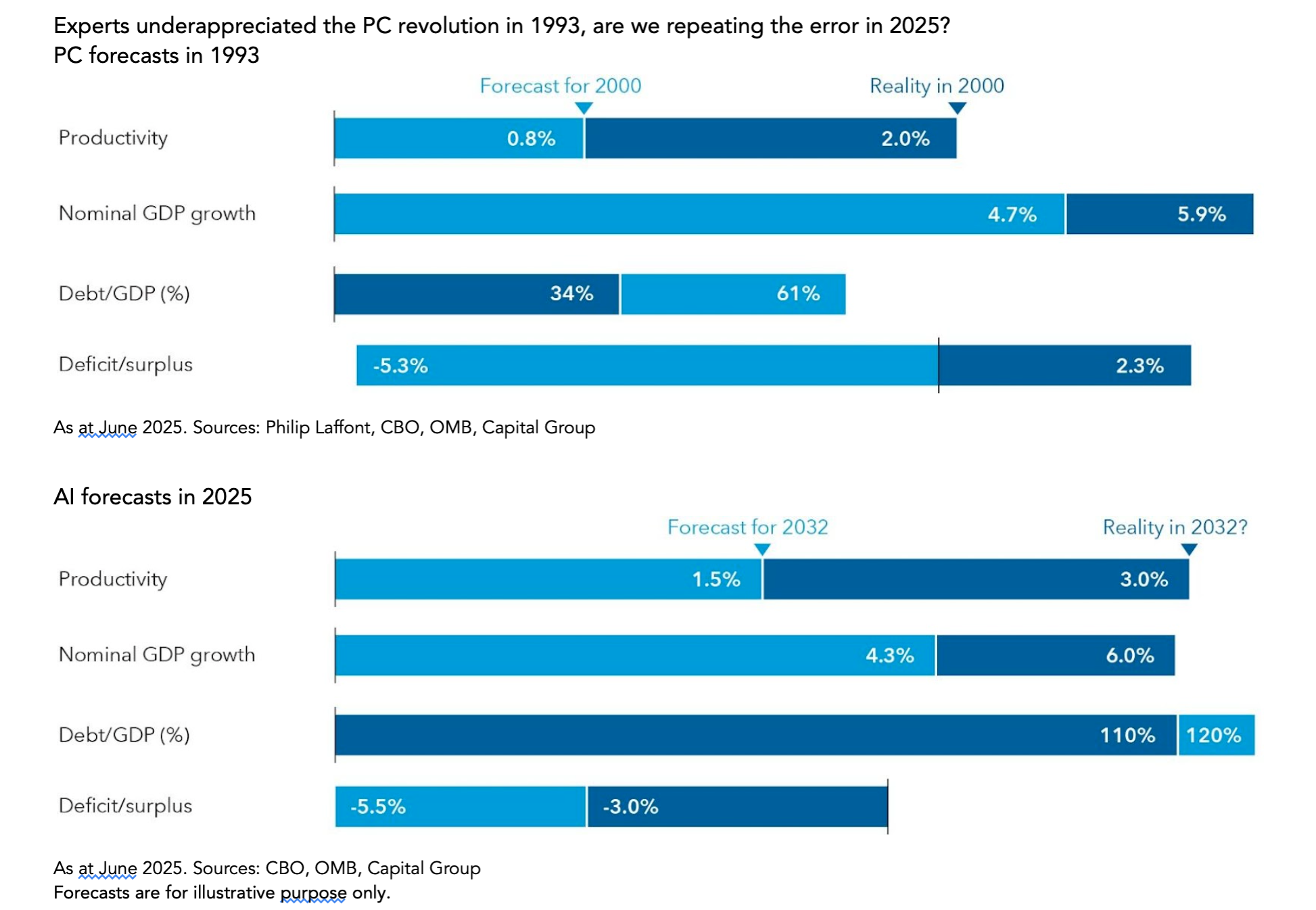

However, a feature of these technologies is that their ultimate impact was generally underestimated. A case study of the personal computing (PC) revolution shows that original estimates of productivity growth and other critical economic measures were far too cautious in hindsight compared with the gains that eventually materialised.

A key question is whether we are making the same mistake today.

Applying the same margin of error from the 1990s to current estimates shows a scenario that would almost double the impact on productivity in addition to positive impacts on other economic indicators.

A key question is whether AI will drive global productivity or if its benefits will be concentrated in a few leading nations. We see three potential scenarios:

- Widely diffused benefits: AI could lift productivity in many countries leading to a new wave of worldwide growth. This would help aging societies mitigate labour shortages and allow developing economies to leapfrog stages of development.

- Concentrated benefit: The advantages of AI might accrue primarily to a few leading nations, particularly the US and China. These countries are at the forefront of AI research and deployment, accounting for the majority of AI startup funding, top talent, and research output.

- Strategic disruption: The country that ‘wins’ the AI race, possibly by achieving Advanced General Intelligence (AGI) first, might use this as a strategic resource, sharing intellectual property only with its allies.

The most likely outcome is that AI will become a general-purpose technology with an uneven rollout. The US and China might be the first to adopt AI at scale, but other nations would benefit with a time lag or in specific areas.

Another critical factor is whether technology and investment move in tandem. If technology advances faster than investment, it could create a major supply shock by disrupting the labour market. At the same time, however, it may deliver major productivity gains in certain tech-oriented sectors.

However, if technological advancements lag investment, the economy has more time to adapt and develop new applications for emerging technology. This would allow continued productive employment across the labour market.

The Goldilocks outcome is one where technology and investments advance together.

AI holds the promise of significantly boosting productivity, and the read-through effects on economic growth and government debt levels could be profound. But its impact will vary across regions and sectors. The strategic adoption and integration of AI will determine which countries and industries reap the most benefits.

Andy Budden is an investment director at Capital Group. He has 33 years of investment industry experience and has been with

Capital Group for 22 years. He holds both a master’s degree and a bachelor’s degree in engineering from the University of Cambridge. He is an associate member of the Institute of Actuaries. Andy is based in Singapore.

Statements attributed to an individual represent the opinions of that individual as of the date published and may not necessarily reflect the view of Capital Group or its affiliates. This communication is intended for the internal and confidential use of the recipient and not for onward transmission to any other third party. This communication is of a general nature, and not intended to provide investment, tax or other advice, or to be a solicitation to buy or sell any securities. All information is as at the date indicated and attributed to Capital Group unless otherwise stated. While Capital Group uses reasonable efforts to obtain information from third-party sources that it believes to be accurate, this cannot be guaranteed.

This communication is issued by Capital International Management Company Sàrl (CIMC), unless otherwise stated, which is regulated by the Luxembourg CSSF – Commission de Surveillance du Secteur Financier.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company. All other company names mentioned are the property of their respective companies.

This article was written in close collaboration with Capital Group.

Read more articles:

Luxembourg Faces Europe’s Defence Reality